VAT (DPH) registration in Slovakia: 4 types — which one to choose

All types of VAT registration for businesses in Slovakia — with examples, current year thresholds and common mistakes. In plain language.

You opened a company in Slovakia, paid for Facebook ads — and suddenly your accountant says you need to register for DPH. The first reaction is panic: reports, a twenty-three percent tax, bureaucracy. In reality, you most likely need a different type of registration than you think. And it’s much simpler than it seems.

In this article, we’ll break down all four types of VAT (DPH) registration in Slovakia — with real-life examples. After reading, you’ll know exactly which type you need.

First, some terminology: IČ DPH, VAT ID and VAT number are all the same thing. Throughout this article, we’ll use the term “VAT number.”

VAT number ≠ VAT payer: two different statuses

The key thing to understand: getting a VAT number in Slovakia doesn’t mean becoming a VAT payer. There are two fundamentally different statuses.

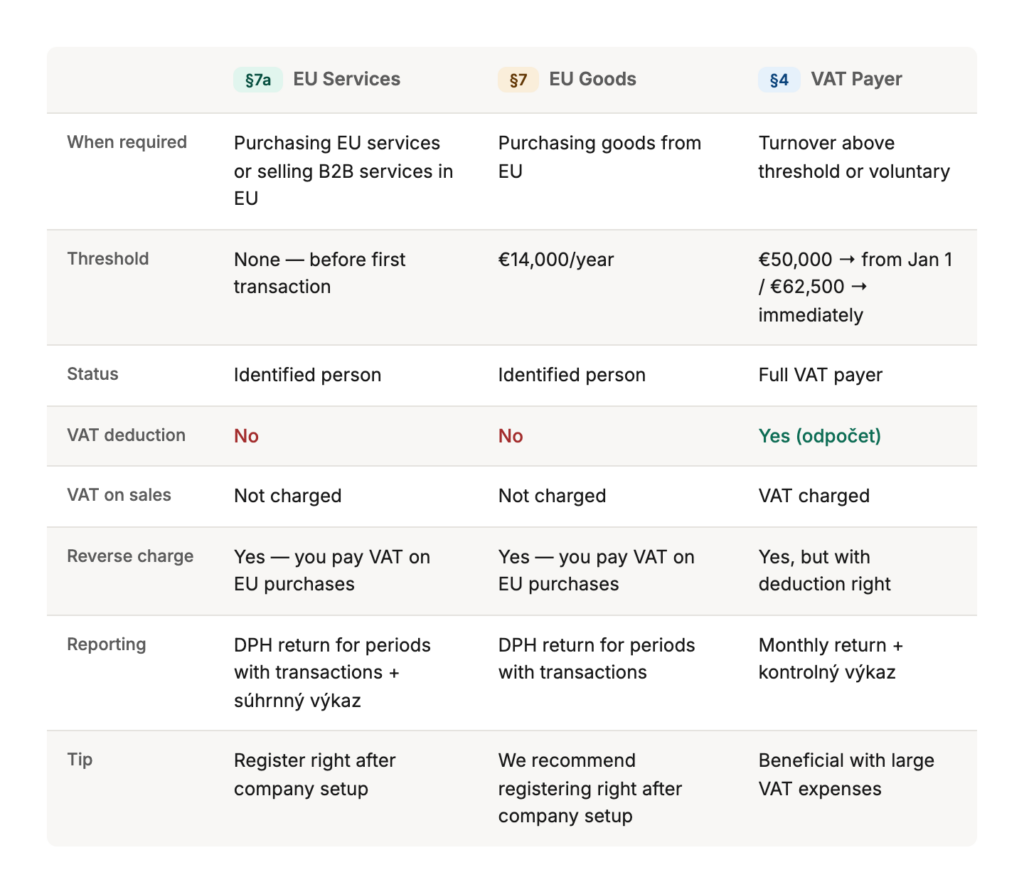

Identified person (identifikovaná osoba, §7 and §7a) — you receive a VAT number, but you don’t become a payer. You pay VAT on your purchases from abroad, but you don’t charge it on your sales. And most importantly — you have no right to deduct input VAT.

VAT payer (platiteľ DPH, §4) — full status. You add VAT to your sales, but in return you can deduct VAT from your expenses (in Slovak — odpočet).

Important: confusion between these statuses is one of the most costly mistakes we see among our clients.

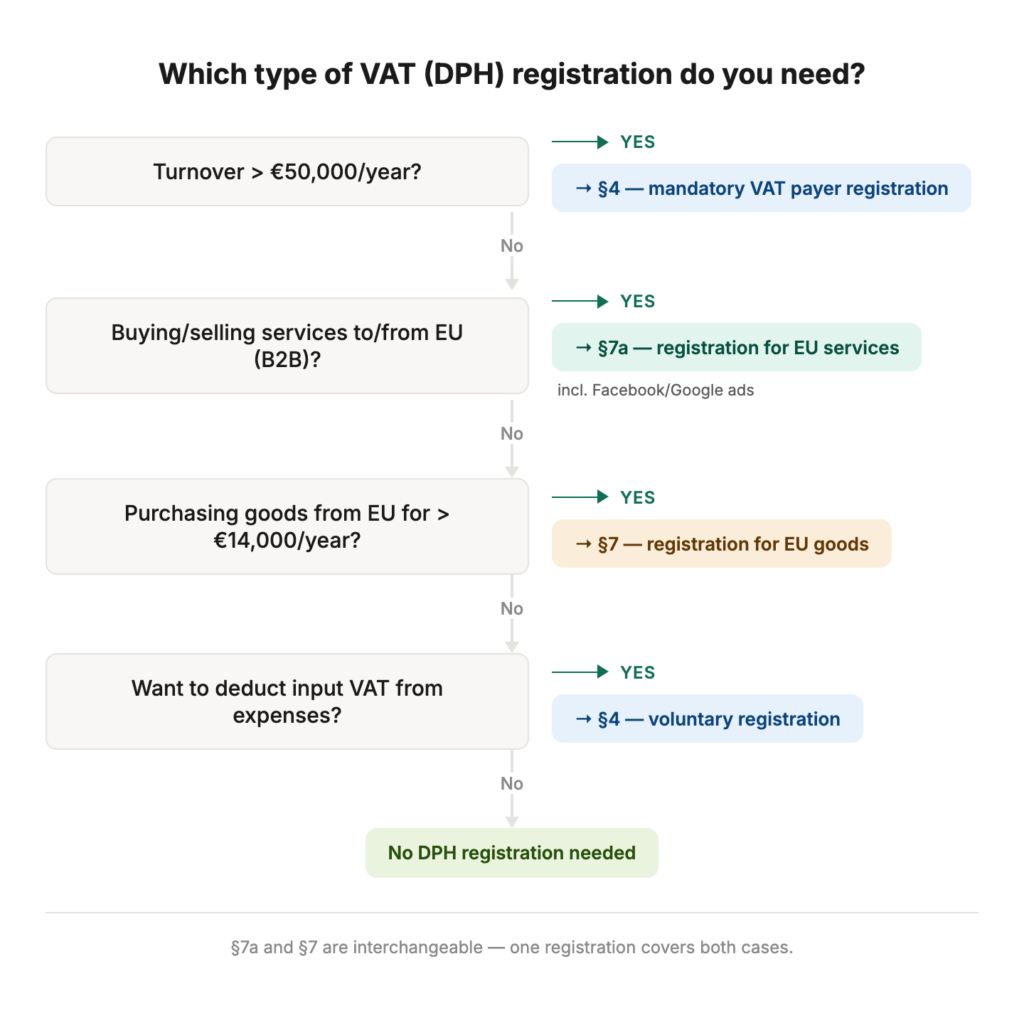

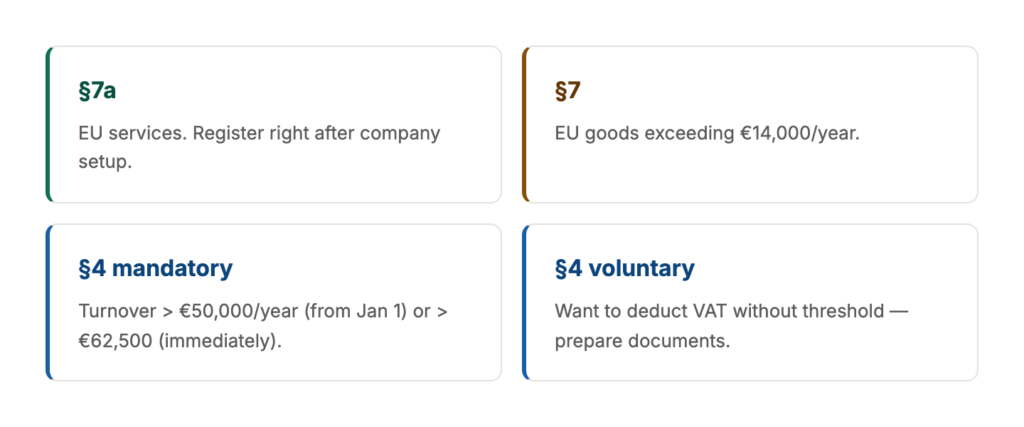

§7a — VAT registration when buying or selling services within the EU

Example: Facebook or Google ads

The most typical case. You run ads on Facebook or Google. Facebook is a company with an Irish VAT number, Google too. This is a service from the EU, which means registration under §7a is required.

What happens without registration? Facebook will issue an invoice with Irish VAT — 23% on top. You pay it. But by law you are also required to charge Slovak VAT on the same transaction and pay it to the budget. That’s double payment.

After registering under §7a you avoid the Irish VAT. But for this you need to enter your VAT number in your ad account settings — simply getting the number isn’t enough, Facebook needs to “see” it.

How §7a works in practice: reverse charge and reporting

When buying services from the EU — you self-assess Slovak VAT (23%) and pay it to the budget. This is called reverse charge (self-assessment). The VAT return (daňové priznanie k DPH) must be filed by the 25th of the following month.

When selling services in the EU to a client with a VAT number — you issue an invoice without VAT and file a súhrnný výkaz (summary report) once a quarter.

Important: you do NOT become a VAT payer. You cannot deduct input VAT from your expenses. You only pay it.

Services from third countries (non-EU)

Paragraph 7a only applies to operations within the EU. If you purchase a service from a third country — for example, from the USA or Ukraine — registration under §7a is not required. But the obligation to charge and pay Slovak VAT at 23% still applies (§69 ods. 3 zákona o DPH).

Tip: if you’ve just opened a company or živnosť and plan to make any purchases from abroad — apply for §7a right away. Registration is free and the number is issued within 7 days. As long as there are no transactions — no reports need to be filed.

§7 — VAT registration when purchasing goods from the EU

Paragraph 7 works similarly to §7a, but applies to goods, not services.

If you purchase goods from other EU countries and the total amount in a calendar year reaches 14,000 euros (excluding VAT), you are required to register. The application must be filed before the threshold is exceeded.

As with §7a, you receive a VAT number but do not become a payer. You pay VAT on the purchase of goods — with no right to deduct.

Important point: if you are already registered under §7a, there is no need to file a separate registration under §7. And vice versa. One registration covers both cases.

§4 — full VAT (DPH) payer registration in Slovakia

Paragraph 4 is the full VAT payer status. Since 2025, significant changes have been introduced here.

New VAT registration thresholds from 2025

Previously the threshold was 49,790€ over a rolling 12 months. Now turnover is calculated per calendar year (January–December), and a two-tier system applies:

First threshold — 50,000€. If you exceed the turnover for a calendar year — you file an application within five business days. You become a payer from 1 January of the following year. There is time to prepare.

Second threshold — 62,500€. If the turnover in the current year exceeds this amount — you become a payer immediately, from the invoice that crossed the threshold. You are already required to charge VAT on it.

Example: your turnover is 60,000€, you issue an invoice for 3,000€ — and from that moment you are a payer. If you find out late — a fine of 100€ to 30,000€.

Right to deduct VAT (odpočet DPH)

The main advantage of payer status is the right to deduct (odpočet) input VAT. Bought equipment, paid rent, purchased goods — the VAT from these expenses can be deducted from what you owe to the state.

Voluntary VAT registration without reaching the threshold

You can register as a payer voluntarily if it is beneficial for you to deduct VAT. However, if the company is not yet active, the tax office may refuse. You will need a business plan, preliminary contracts and invoices — preferably from Slovak counterparties. If the company already has turnover — it’s easier. If turnover is approaching the threshold — there are usually no issues.

Common mistakes when registering for VAT in Slovakia

Mistake #1: VAT exceeds the company’s income

The company is registered under §7 or §7a and purchases goods or services from the EU in large volumes. With these registrations there is no right to deduct — the VAT on top becomes a pure expense. We have seen cases where the total VAT exceeded the company’s entire income.

What to do? It depends on the business model. If you sell B2B — it’s worth considering full registration under §4. More reporting, but you get the deduction. If you work B2C — the situation is different: as long as you’re not a payer, you don’t add VAT to your prices, and your price for the client is lower than a competitor who is a payer. Each situation should be calculated separately.

Mistake #2: forgot to file the return and pay VAT

You registered under §7a, purchased a service from the EU — and forgot to file the return and pay the assessed tax. The result — a fine for non-filing plus the obligation to pay the tax amount itself along with penalties.

Mistake #3: confusing the VAT number with payer status

“I have an IČ DPH, so I’m a payer!” — No. A VAT number under §7 or §7a is not payer status. It is identification for specific transactions. You cannot deduct VAT.

Bonus: mixed activity and the deduction coefficient

If your company is a payer under §4 and carries out both taxable and VAT-exempt activities simultaneously (for example, financial services), the input VAT deduction must be reduced proportionally. This is called koeficient. There are many nuances, and in each case it’s worth consulting your accountant.

Quick cheat sheet on DPH registration types

This article is for informational purposes only and does not constitute tax advice within the meaning of Act No. 78/1992 Zb. on daňových poradcoch. For individual recommendations, please consult a licensed tax advisor (daňový poradca).

If you have a specific situation and need help with accounting — contact us. We also offer free online tax return forms for entrepreneurs in Slovakia.